The Biden-Harris Administration provided a historic $24 billion in subsidies to the child care industry through the March 2021 enactment of the American Rescue Plan (ARP). This unprecedented investment helped to stabilize the provision of child care during the pandemic while also helping to address preexisting challenges in the market. These resources were used by child care providers to retain staff, pay rent, and keep the lights on during uncertain times. This blog summarizes a new CEA working paper, which shows that these funds succeeded in slowing cost growth for families, stabilizing employment and increasing wages for child care workers, and increasing maternal labor force participation. These investments had a benefit-cost ratio of about 2:1, meaning the benefits of these funds for the broader economy outweighed the costs of investment.

To continue the success of this unprecedented investment, the Administration has transmitted a supplemental request to Congress that includes an additional year of child care stabilization funding. Our analysis strongly suggests that failing to re-up this investment could reduce the supply of care available to families, which has the potential to stall the important progress we document below. This stalling could cause child care providers to raise prices, serve fewer families, and even close altogether.

Savings for Families: Child care prices moved in lockstep with those of other goods and services before the ARP stabilization funds were distributed but slowed after the onset of funds. By comparing the growth of child care prices to the growth of similar prices after the distribution of funds, we estimate that child care prices were 10 percent lower than they would have been absent ARP funds. This translates to savings of about $1,250 per child, or a nearly 10 percent savings on the annual average price families pay for care. These savings provided meaningful relief at a time in which it is estimated that a U.S. couple both making the minimum wage would need to spend roughly 40 percent of their combined income on child care.

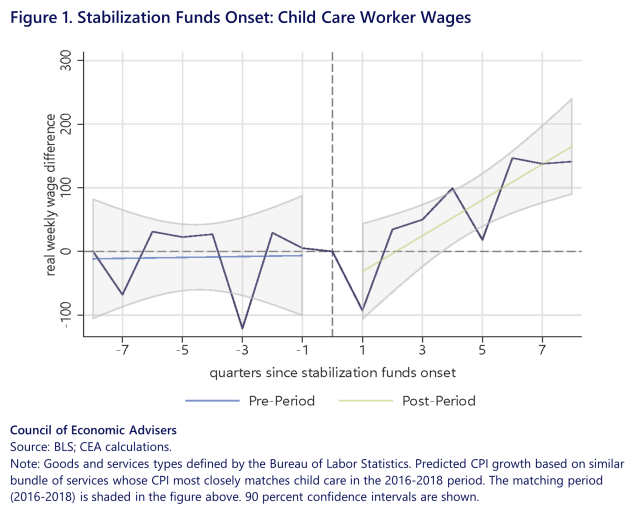

Higher Wages and More Employment in Child Care: Many states and localities report using large portions of their ARP stabilization funds to provide bonus and retention pay to child care workers, a group disproportionately comprised of women and people of color, and whose wages are historically close to minimum wages. To estimate the effect of stabilization funds on the wages of child care workers, we compared the change in wages for child care workers after the funds were made available to those of primary and secondary school teachers (K-12 teachers) during the same time period. Figure 1 shows the difference between child care worker wages and K-12 worker wages before and after ARP stabilization (centered at zero). Before stabilization, the wage gaps between workers in the two industries were largely stable. However, after stabilization, there was a clear relative increase in weekly wages for child care workers of about $3,800 annually relative to what wages would have been absent the ARP. This represents a roughly 10 percent increase in child care worker wages.

Using a similar approach for child care employment relative to K-12 workers, we find that child care employment increased by roughly 7 percent between the onset of ARP funds and the first quarter of 2023. Given the tight link between the number of staff and children served in child care due to requirements around the minimum ratio of children per adult, one could reasonably conclude that ARP stabilization funds led to a similar increase in child care slots (relative to what it would have been absent the ARP).

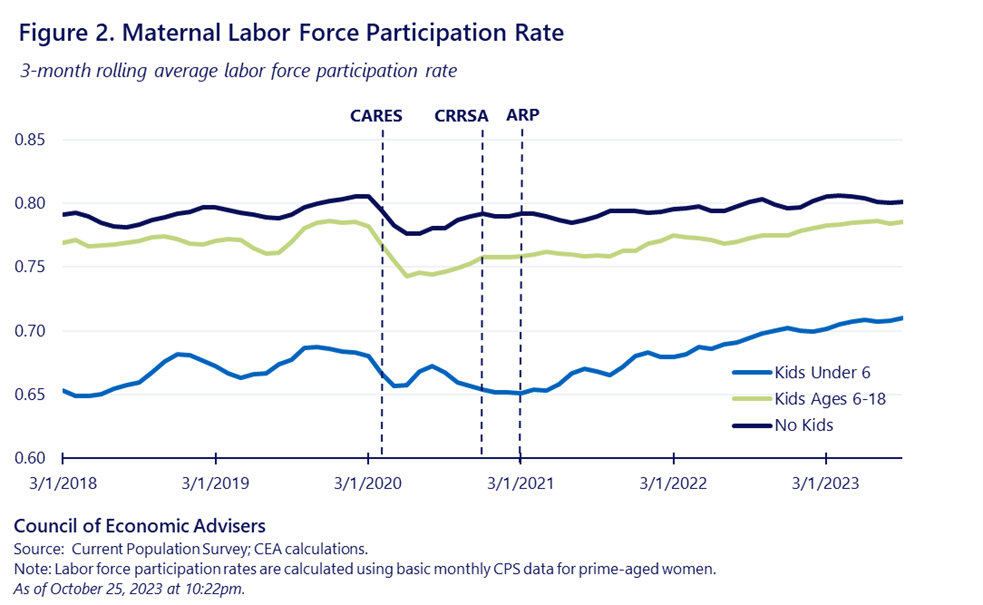

More Mothers in the Labor Market: The child care industry primarily serves children under the age of 6, while most children 6 and older attend primary and secondary school.[1] If the cost and accessibility of child care constrains parents, especially mothers, in their ability to work, then the stabilization induced by the ARP funds should increase the labor force participation of mothers with young children (under the age of 6). Based on this insight, we examined the change in outcomes for mothers of young children before versus after the stabilization funds were dispersed. To isolate the effect of stabilization, we use mothers of older children (between the ages of 6 and 18) as a comparison group. This approach essentially accounts for factors that would affect all mothers similarly, such as the popularization of work-from-home policies.

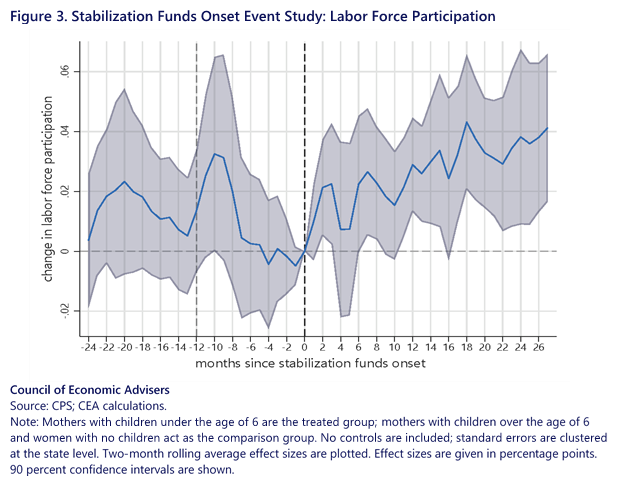

Figure 2 shows that before the distribution of stabilization funds, the trends in the labor force participation of mothers with young children was similar to that of other women–indicating that mothers of older children and women with no children provide a relevant comparison point for mothers of young children. Figure 3 plots the difference in labor force participation rates between mothers of young children and other women before and after ARP funds were distributed. While the difference between the two groups was largely unchanged in the months before ARP funds were distributed, after they were distributed the labor force participation of mothers with young children increased relative to other women by about 3 percentage points. This is exactly what one would expect if the stabilization funds facilitated greater access to affordable child care, which in turn facilitated mothers’ return to work. Providing compelling evidence that this effect is causal, we find that the increased labor force participation rate associated with stabilization funds slowed around the time when counties received their final funds payout from states.

ARP Child Care Stabilization Funds Were Very Cost Effective: As of June 2023, approximately $20 billion of ARP stabilization funds had been distributed to child care programs. Our estimates suggest that this led to the labor force participation of roughly 325,000 mothers of young children, representing an additional $26 billion in earned wages. The $3,800 annual pay increase for about 950,000 child care workers over two years is a total of $7.2 billion, and about $1.9 billion in additional earnings accrue to newly hired child care workers. The savings to families for the roughly 4.2 million children in child care is approximately $5.3 billion. These gains total to $40.4 billion in benefits compared to a $20 billion total outlay during the period over which we measure benefits–a benefit-cost ratio of 2:1. Moreover, we estimate that about 40percent of these ARP stabilization dollars will likely be recouped by the government in the form of tax revenues and reduced benefit spending.

Looking forward: Although ARP stabilization funds have contributed to immense progress across the child care industry, the market still operates at a deficit. As funds expire, a persistent deficit could cause a market contraction with the potential to stall this progress. This stalling could cause child care providers to raise prices, serve fewer families, and even close altogether.

Evidence of stalled progress is visible in counties that have already spent down their funds. This evidence, along with that presented in the full working paper, underscores the importance of continued investment in the child care industry. The Administration’s fiscal year 2024 Budget takes seriously the importance of continued support with transformational investments to expand access to high-quality child care and preschool. And the Administration continues to call on Congress to provides the resources needed to prevent families from losing critical child care.

[1] Acknowledging that many families rely on non-parental care arrangements before and after school, however, these arrangements tend to be more limited in time and are less costly than those provided to children aged zero to five.

{kind=link}