In the past, handling family finances was often seen as the responsibility of the man of the house. Fortunately, that kind of thinking is as antiquated today as black-and-white TVs and rotary phones.

But this doesn’t mean that women today are adept at managing their own money (not that all men are either). One glaring reason for this, says HelpAge USA, a Washington, D.C.-based advocacy group, is that opportunities for financial education for many women are lacking.

In a report — conducted with the University of Southern California’s Dornsife Center for Economic and Social Research and funded by the Robert Wood Johnson Foundation — it notes that more than 70% of U.S. women aged 40–65 want to get some sort of financial education, with demand among Black, Hispanic/Latina, and Asian women especially high. But few — just 16% — have ever gotten it.

“There is a common myth that older people, and especially older women, are not interested in financial education or that this demographic lacks financial value,” says Cindy Cox-Roman, HelpAge USA’s president and chief executive. “However, our research and international experience shows that this is not the case.”

The study found that average financial literacy scores for men were 25% higher than for women, even though cognitive scores were not statistically different by gender, and this gap persisted even after controlling for education and employment status.

It’s not like programs to boost financial literacy for women don’t exist. They just don’t exist for older women. The HelpStudyUSA/USC study notes an analysis by the Kaiser Family Foundation showing that of 76 financial programs it reviewed, “few focused on the population aged 50+ and only one on older women.”

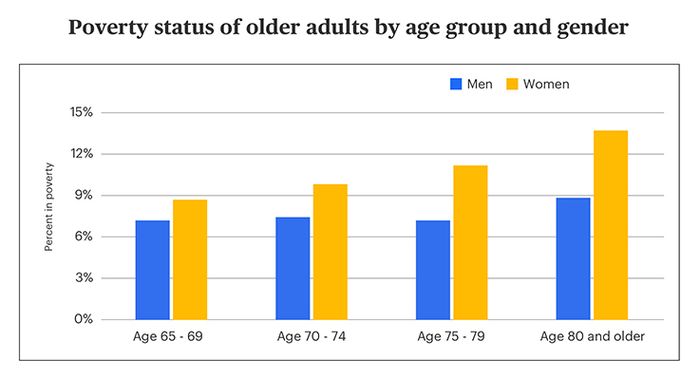

This financial literacy gap is evident in statistics like average 401 (k) balances, which are 50% higher for men ($89,000) than women ($59,000) according to a recent Bank of America study. To be fair, other issues play a role, such as wage discrimination and career interruptions to raise children, dynamics that still fall preponderantly upon women. Even so, the relative lack of knowledge when it comes to critical skills like personal finance and retirement saving looms large. This in turn, feeds discouraging statistics that rear their ugly heads later in life, such as the fact that greater percentages of women live in poverty than men.

Federation of American Scientists

What can be done? For starters, we would do well to study the best practices found elsewhere. Cox-Roman tells me about a program in Singapore, called the Citi-Tsao Foundation Financial Education Programme for Mature Women. After looking at it myself, I agree that it is intriguing.

Like America, Singapore, a tiny high-tech powerhouse in Asia, is a rapidly aging country. By the year 2030, its government says, one in five citizens will be age 65 or older — a figure comparable to here. And, like here, women tend to be in more dire financial situations than men.

That’s where the Citi-Tsao program comes in. Launched in 2008, it targets low-income women above age 40, exposing them to a specially-tailored curriculum which runs about two hours a week for 12 weeks. “Through these sessions,” the program’s outline says “participants are taught about savings and planning for the long term, budgeting and investing.” The goal is obvious: “to provide practical suggestions for understanding how money works and how women can take charge of their finances to become more financially independent and secure as they grow older.”

This isn’t rocket science, just basics that can go a long way in boosting financial acumen and the confidence that goes with it.

And it seems to work, Cox-Roman says.

“Significantly, a follow-up evaluation of the Citi-Tsao program found that the women aged 40–60 who participated in the program reported feeling more control and reduced stress related to financial decision-making 10 years later. Building women’s financial health at older ages is critical to our mission of advancing the dignity and well-being of older people and cannot be overlooked.”

There’s no reason that federal and state governments, working with financial and education institutions, can’t develop something similar here. Given things like the strains on Social Security and Medicare, rising healthcare costs, and an overall dearth of retirement savings, time is of the essence. Joanne Yoong, a USC research fellow says something like Citi-Tsao could be scaled up here and made accessible to anyone who wants it. “There is a significant opportunity to empower older women with the financial literacy skills they want and need.“